Save

Save Print

Print

Restocking demand, Australian weather and the strength in global steel demand recovery are likely to drive seaborne coking coal prices in the Asia-Pacific in coming weeks after the spot market fell below $250/t fob Australia in November.

The Australia low-volatile premium hard coking coal price has fallen by over $64/t, or 21pc, from the start of the month to $247.45/t fob on 30 November. The drop was caused by factors similar to those seen in July when the index fell by $105/t or 35pc over the month.

Demand took a hit last month as mills cut production because of poor margins. Spot availability also improved after more end users emerged to resell their long-term cargoes.

Falling offer levels on the Globalcoal screen also fuelled buyers' anticipation of a further price weakness. Most end users did not want to risk buying spot cargoes as they had sufficient inventory. Weak demand was also underlined by offers of pulverised coal injection (PCI) from end users in the spot market.

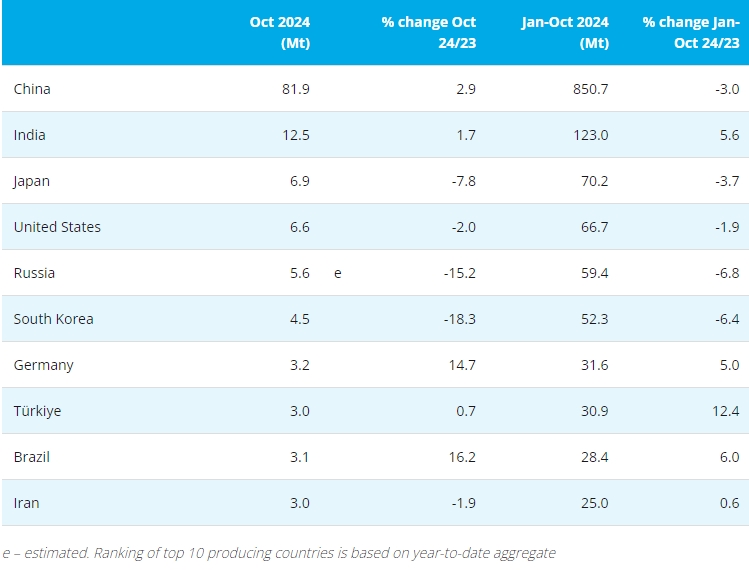

"First quarter prices should be stable around $250/t levels as there is demand from India, although Europe's demand is weak," a Singapore-based trader said. India produced 10.5mn t of crude steel in October, up by 2.7pc on the year, while January-October output was at 103.8mn t, up by 6.1pc on the year. The EU produced 11.3mn t of crude steel in October, down 17.5pc on the year while January-October output was down 9.2pc on year to 117.1mn t.

An Indian trader agreed that prices could remain rangebound, but cautioned that the weather and thermal market could provide a floor to prices and even push them higher.

"Fob Australia prices should remain stable, on the condition that the weather in Australia is good," the trader said. "Otherwise, prices will spike in another month or so when it is the high tide for monsoon." Australian hard coking coal exports were at 79mn t in January-September this year, down by 6pc from a year earlier. Exports of PCI and semi-soft coking coal were at 39mn t, down by 6pc on the year. Australian hard coking coal exports are on track to register a fourth consecutive year of decline.

The trader also highlighted the possibility of tighter coking coal supply as the market could see crossover volumes into the thermal sector, especially if winter demand for thermal coal supports prices.

The Argus daily fob Australia premium low-vol index was at $249.45/t on 2 December. Prices climbed as consecutive premium hard coking coal trades hovered around $245-249/t fob Australia. Most participants pointed out that prices have bottomed out and restocking needs have emerged, with spot enquiries from major Indian steel mills for next quarter's cargoes.

Some other participants hold a conservative outlook, pointing that global downstream demand remains weak, and India alone cannot sustain the demand for coking coal.

"The only place with increasing steel demand is India," a trader said. "Construction and automobile sectors are doing well, but this itself cannot change the entire market dynamics. We will need support from China and Europe." Another trader pointed out that market fundamentals in India were not as strong as expected despite sentiment improving after the removal of export duties on steel products.

argusmedia

Copyright © 2013 Ferro-Alloys.Com. All Rights Reserved. Without permission, any unit and individual shall not copy or reprint!

- [Editor:kangmingfei]

Daily News

Daily News Research

Research Magazine

Magazine Company Database

Company Database Customized Database

Customized Database Conferences

Conferences Advertisement

Advertisement Trade

Trade

Tell Us What You Think